Introduction

In the spring of 2022, diesel prices in the United States rose at a pace not seen in decades. According to the U.S. Energy Information Administration, the national average on-highway diesel price increased from roughly $3.60 per gallon in January 2022 to more than $5.70 by June, which is the highest nominal level on record at the time. The Bureau of Transportation Statistics classified the surge as part of the largest sustained motor fuel price increases in recent history.

As fuel costs climbed, many assumed vehicle shipping rates would rise proportionally and immediately. That assumption warrants closer examination.

Between 2019 and 2025, diesel prices moved through three phases: pre-pandemic stability, pandemic contraction, and post-pandemic inflationary expansion. During the same period, transportation cost indices increased, labor costs rose, carrier capacity fluctuated, and seasonal demand cycles intensified.

To evaluate diesel’s role within that broader environment, we analyzed six years of federal diesel data from the EIA and FRED, along with transportation and labor indices from the Bureau of Labor Statistics. These datasets were compared with route-level pricing across several high-volume corridors, including Texas–Florida, New York–Florida, and Texas–California.

The results show that diesel and auto transport rates do not move in a simple one-to-one relationship. On long-haul routes, fuel sensitivity compounds over distance. During peak seasonal demand, however, capacity constraints often outweigh fuel fluctuations. In multiple periods between 2021 and 2023, route-level pricing adjustments lagged diesel movements by several weeks.

Diesel is a meaningful cost driver in auto transport, but not the only one.

Data Sources & Methodology

This analysis covers the period from January 2019 through the most recent available 2025 data in order to capture three distinct pricing environments: pre-pandemic stability, pandemic-driven contraction, and post-pandemic inflationary expansion. Establishing 2019 as a baseline allows comparison against both the COVID-era demand shock and the inflationary fuel cycle that followed.

Rather than relying solely on published summaries, we constructed a multi-layer dataset combining federal diesel statistics, freight and labor cost indices, and route-level pricing records.

Diesel Price Data

We compiled weekly U.S. on-highway diesel price data from the U.S. Energy Information Administration (EIA) [1] and verified historical consistency using the Federal Reserve Economic Data (FRED) series GASDESW [4]. Extended historical datasets were retrieved through the EIA retail diesel portal [2].

To ensure analytical alignment with transport pricing cycles, wfeekly diesel prices were converted into monthly averages. This allowed direct comparison with monthly route-level pricing data and reduced distortion from short-term weekly volatility.

In addition to national averages, we reviewed regional diesel spreads using Department of Energy (DOE) regional pricing data to evaluate structural cost differences between Gulf Coast, Midwest, Northeast, and West Coast markets. These regional differentials were later incorporated into route-level sensitivity analysis.

Freight and Cost Context

To prevent fuel from being treated as an isolated variable, we incorporated broader transportation cost indicators from the U.S. Bureau of Labor Statistics (BLS), including transportation service cost indices [7] and unit labor cost measures for service-providing industries [8].

Freight capacity cycles were further contextualized using freight-related economic series from FRED [5], supplemented by industry summaries from the American Trucking Associations [10].

These datasets allowed us to evaluate whether observed rate movements aligned with fuel changes alone or coincided with broader cost and capacity pressures.

Route-Level Pricing & Statistical Testing

National fuel data was then compared with monthly average open auto transport pricing across three high-volume corridors: Texas to Florida, New York to Florida, and Texas to California.

For each route, we calculated average price per mile using anonymized shipment data and grouped results by calendar month. Seasonal patterns were segmented into peak (October–March) and off-peak (April–September) periods to isolate demand-driven pricing from fuel-driven movement.

To quantify diesel’s influence, we conducted correlation analysis between monthly diesel averages and route-level pricing. In addition, we performed lag testing by comparing diesel movement in a given month with transport rate adjustments in subsequent months. This approach allowed us to determine whether pricing responded immediately to fuel volatility or followed with a measurable delay.

We also calculated estimated fuel sensitivity ranges by evaluating how incremental diesel changes corresponded with per-mile rate adjustments across each corridor. These calculations form the basis of the route-specific findings presented in later sections.

By combining federal fuel data, labor indices, freight indicators, and proprietary route-level pricing records, this study moves beyond descriptive fuel trends to quantify how, when, and to what extent diesel prices influence auto transport costs.

National Diesel Price Cycle (2019–2025)

Before examining route-level transport pricing, it is necessary to establish how diesel prices moved nationally between 2019 and 2025. Diesel represents a primary operating expense for vehicle carriers, but its influence must be measured against documented fuel cycles rather than assumptions.

Using weekly U.S. on-highway diesel data from the U.S. Energy Information Administration (EIA) [1], cross-verified with the Federal Reserve Economic Data (FRED) GASDESW series [4], we reconstructed the national diesel pricing trajectory from January 2019 through early 2025.

The data reveals five distinct phases.

.jpg)

2019: Pre-Pandemic Baseline

Throughout 2019, national average diesel prices generally fluctuated between approximately $2.90 and $3.20 per gallon, according to EIA historical retail diesel data [2]. Monthly volatility remained moderate, and price swings were relatively contained compared to subsequent years.

From an operational standpoint, this period reflects a structurally stable freight environment. Carrier pricing was predictable, fuel surcharges were manageable, and long-haul lane pricing did not require frequent adjustment due to fuel instability.

2020: Pandemic Contraction

Between January and May 2020, diesel prices declined sharply. EIA weekly data indicates national averages fell from roughly $3.05 per gallon in early January 2020 to approximately $2.40 by late May; a decline of approximately 20% within five months (EIA, Historical Retail Diesel Data).

This drop coincided with widespread economic contraction and reduced freight demand.

However, route-level transport pricing did not decline in perfect proportion or with immediate timing. Carrier rate adjustments often lagged diesel movement due to contractual commitments, dispatch cycles, and uncertainty within the freight market.

The 2020 contraction illustrates that diesel can move rapidly, while transport pricing typically adjusts more gradually.

2021: Sustained Recovery

Beginning in early 2021, diesel prices began a sustained upward trend. From pandemic lows near $2.40 per gallon, national averages climbed steadily throughout the year, reaching approximately $3.60 by late 2021 (EIA; FRED GASDESW series).

This represents roughly a 50% increase from the 2020 trough.

Unlike the abrupt decline in 2020, the 2021 recovery unfolded gradually. Carriers adjusted pricing incrementally, particularly on longer corridors where fuel sensitivity compounds over distance. Spot market volatility increased, but pricing changes generally reflected sustained cost pressure rather than sudden disruption.

2022: Inflationary Surge

The most significant diesel movement in the study period occurred in 2022. According to EIA weekly data, national diesel prices increased from approximately $3.60 per gallon in early January 2022 to more than $5.70 by June 2022 (EIA, Weekly Diesel Prices). The Bureau of Transportation Statistics classified this period as part of the largest sustained motor fuel price increase in recent history [6].

From January to peak, diesel increased approximately 60% in less than six months.

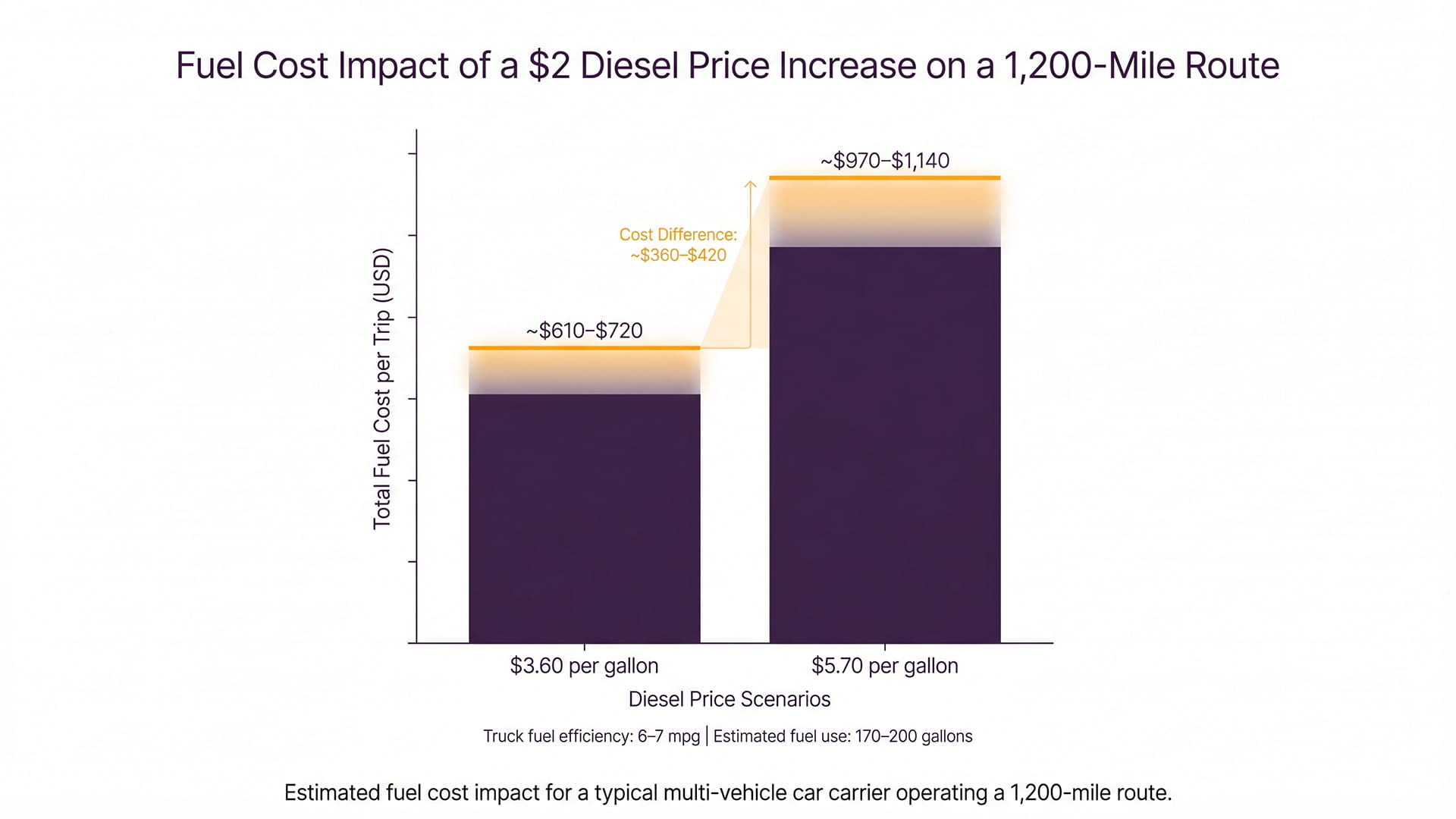

For multi-vehicle carriers operating long-haul corridors, this magnitude of change materially altered trip economics. A sustained increase of over two dollars per gallon significantly impacts fuel expenditure across 1,000+ mile routes.

To illustrate the scale of this shift, a typical multi-vehicle car carrier averaging roughly 6–7 miles per gallon would consume approximately 170–200 gallons of diesel on a 1,200-mile route. A $2.00 increase in diesel prices therefore raises fuel expenses by roughly $340–$400 per trip, depending on equipment efficiency and regional fuel pricing.

Load boards reflected tightening conditions before many contracted transport rates were formally adjusted. In several corridors, route-level pricing peaks followed diesel highs with measurable delay, suggesting lagged cost pass-through rather than instantaneous repricing.

The 2022 surge represents the largest fuel shock within the 2019–2025 study window.

2023: Partial Normalization

In 2023, diesel prices declined from their 2022 peak but remained elevated relative to pre-pandemic levels. National averages frequently fluctuated between approximately $4.00 and $4.50 per gallon during much of the year (EIA Historical Data; FRED GASDESW).

Although volatility subsided compared to 2022, pricing did not return to the 2019 baseline range of $2.90–$3.20. Structural operating costs across the freight sector remained higher, supported by continued labor cost increases documented by the U.S. Bureau of Labor Statistics [7].

2024: Elevated Stability

Monthly EIA data for 2024 indicates continued fluctuation within a narrower band compared to the 2022 spike, yet materially above 2019 norms [3].

Extreme volatility was absent. However, the structural pricing floor remained elevated.

By this stage, carriers increasingly incorporated higher assumed fuel costs into baseline lane pricing rather than treating elevated diesel levels as temporary anomalies.

2025: Early Observations

Preliminary 2025 data from EIA and related federal updates suggests continued fluctuation around elevated post-2022 levels (EIA Weekly Data; FRED GASDESW). While short-term movements persist, the broader pattern indicates that the sub-$3 diesel environment characteristic of 2019 has not returned.

The structural baseline has shifted.

Observations from the National Diesel Cycle

Between 2019 and 2025, diesel prices moved from relative stability near $3.00 per gallon to a pandemic low near $2.40, then surged above $5.70 before settling into an elevated post-2022 range.

The difference between the 2020 trough and the 2022 peak represents more than a doubling in absolute fuel cost within a two-year window.

However, as later sections will demonstrate, diesel movements did not always produce proportional or immediate changes in auto transport rates. In several periods, pricing adjustments lagged fuel volatility. In others, broader freight and labor pressures amplified or dampened diesel’s influence.

With the national fuel cycle established using documented federal data (EIA; FRED; BTS), the next step is to evaluate the broader freight and cost environment that coexisted with these fuel movements and determine whether diesel operated as the primary driver of auto transport pricing or as one variable within a more complex system.

Transportation Service Cost Indices

BLS service-providing industry data [7] shows transportation-related service costs rising steadily from 2021 through 2023, following a temporary contraction in 2020.

The index declined during the early pandemic period, consistent with reduced freight activity. However, beginning in late 2020 and accelerating into 2021, transportation cost indices began trending upward and remained elevated through 2022 and 2023.

This upward movement occurred even during periods when diesel prices temporarily stabilized or declined.

For example, while diesel eased in parts of 2023 relative to the 2022 peak (EIA weekly diesel data), transportation cost indices did not return to pre-pandemic levels. This divergence indicates that non-fuel operating costs remained structurally elevated.

The implication is measurable: if route-level pricing remained firm during periods of diesel moderation, fuel alone cannot explain that behavior.

Labor Cost Component

Unit labor cost data from the BLS [8] shows sustained upward pressure across service-providing sectors beginning in 2021.

Unlike diesel, labor costs do not exhibit sharp weekly volatility. Instead, they rise incrementally across quarters. From 2021 onward, unit labor indices in transportation-adjacent industries increased alongside broader inflationary pressures.

This matters for one specific reason: labor cost increases are rarely reversed in short cycles.

When diesel fell in late 2022 and portions of 2023, labor indices did not fall proportionally. As a result, baseline operating cost structures remained elevated even as fuel moderated.

That structural persistence provides context for why route-level pricing did not fully retrace 2022 peaks in direct proportion to diesel declines.

Freight Market & Capacity Indicators (2019–2025)

Diesel prices alone cannot explain how vehicle transport rates evolve. To understand pricing behavior across the auto transport market, we also examined freight demand cycles and trucking capacity indicators that influence carrier availability.

For this purpose, we reviewed data from the Cass Freight Index [9], the American Trucking Associations (ATA) Truck Tonnage Index, and several freight-related economic series tracked through Federal Reserve Economic Data (FRED). These indicators provide a broader view of how freight demand and trucking activity moved alongside fuel prices.

The Cass Freight Index [9] shows a sharp contraction in shipment volumes during early 2020 as pandemic disruptions reduced economic activity. Freight demand then rebounded strongly through 2021 as supply chains restarted and goods consumption accelerated. During that recovery phase, trucking capacity tightened and freight expenditures increased across multiple sectors.

.jpg)

Data from the ATA Truck Tonnage Index [10] reflects a similar pattern. Tonnage declined during the early pandemic period before recovering through 2021, followed by slower growth in 2022 and moderation through 2023 as freight demand normalized.

When these indicators are examined alongside diesel prices, the relationship becomes clearer. Fuel costs increased significantly in 2022, but freight capacity conditions also played a role in how quickly those costs translated into transport pricing.

Our analysis suggests that fuel volatility alone does not determine vehicle transport rates. When freight demand is strong and carrier availability tightens, cost increases tend to appear in shipping prices more quickly. Conversely, during periods of weaker freight demand, diesel movements may take longer to influence pricing.

Route-Level Price Sensitivity Analysis

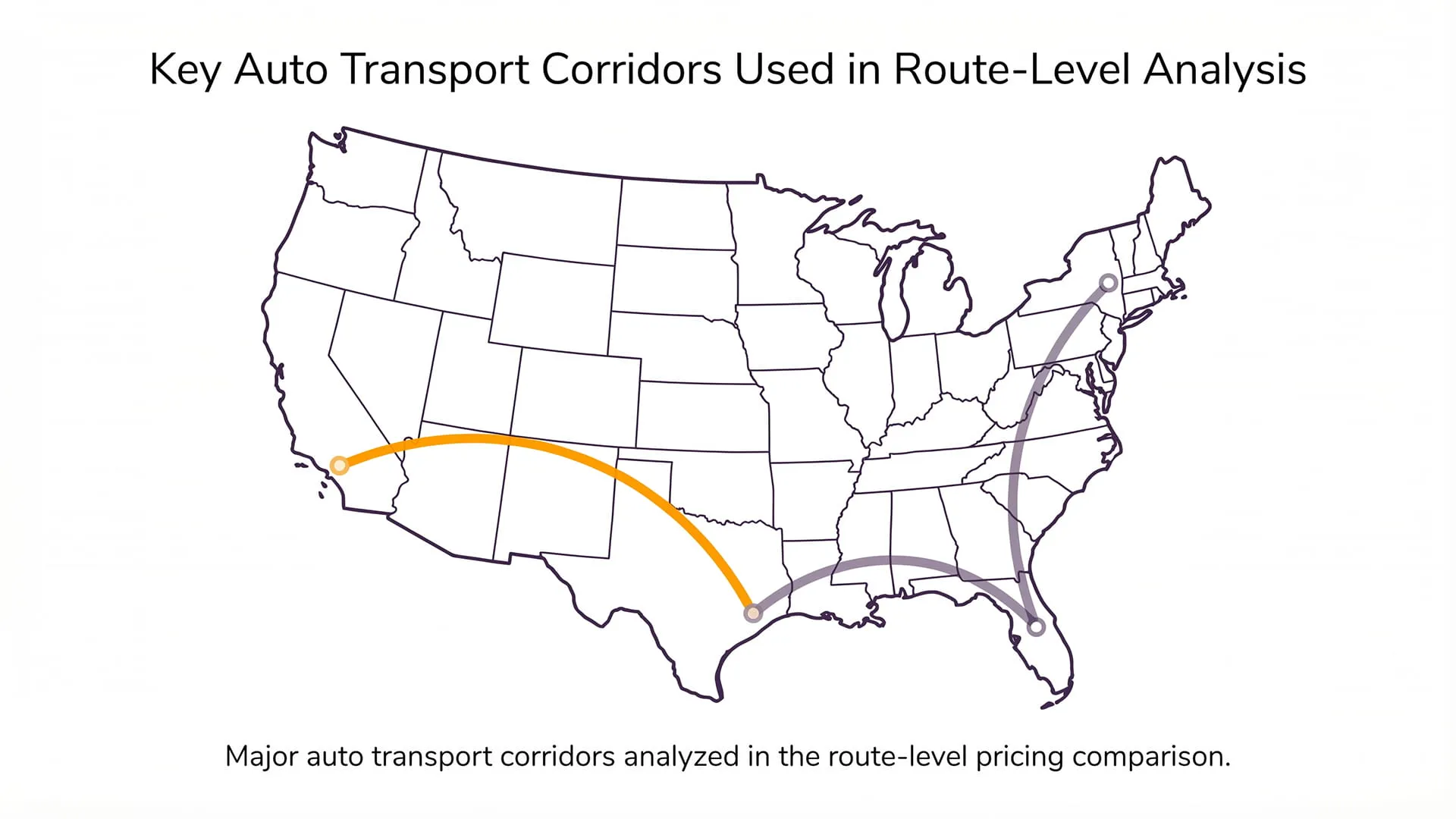

To evaluate how diesel price movements translate into real shipping costs, we compared monthly route-level pricing across three high-volume corridors: Texas → Florida, New York → Florida, and Texas → California. These routes represent different transport dynamics, including seasonal relocation demand and long-haul fuel sensitivity.

Texas → Florida

The Texas to Florida corridor is one of the most stable long-haul vehicle transport routes in the United States. Demand is consistent due to relocation traffic, dealership movement, and seasonal migration.

Our analysis shows that diesel price increases generally affect this corridor gradually rather than immediately. Because the route has consistent carrier availability and frequent backhaul opportunities, pricing adjustments tend to occur incrementally as carriers adjust fuel assumptions in lane pricing.

During the 2022 diesel surge, route pricing increased, but the adjustment followed fuel movements with a short delay rather than moving in direct weekly correlation.

New York → Florida

The New York to Florida corridor is heavily influenced by seasonal snowbird migration, particularly between October and March.

In this corridor, demand cycles often outweigh fuel movements. During peak winter relocation periods, transport prices increased even when diesel prices remained relatively stable. Conversely, during off-season months, price moderation occurred despite elevated diesel levels.

This pattern indicates that capacity constraints during peak migration periods can amplify pricing more than fuel volatility alone.

Texas → California

The Texas to California corridor represents a longer westbound lane where fuel sensitivity becomes more pronounced due to distance.

Across this route, diesel fluctuations had a clearer relationship with per-mile transport pricing. When fuel prices rose significantly in 2022, the cost increase was reflected more directly in route pricing compared with shorter corridors.

However, even on this long-haul lane, diesel was not the only driver. Freight demand and carrier availability still influenced how quickly rate adjustments appeared.

Cross-Country Benchmark (Optional)

Cross-country lanes such as California → New York demonstrate the strongest combined influence of distance and capacity cycles. On these routes, diesel price increases compound over longer mileage, while limited carrier availability can further intensify pricing during high-demand periods.

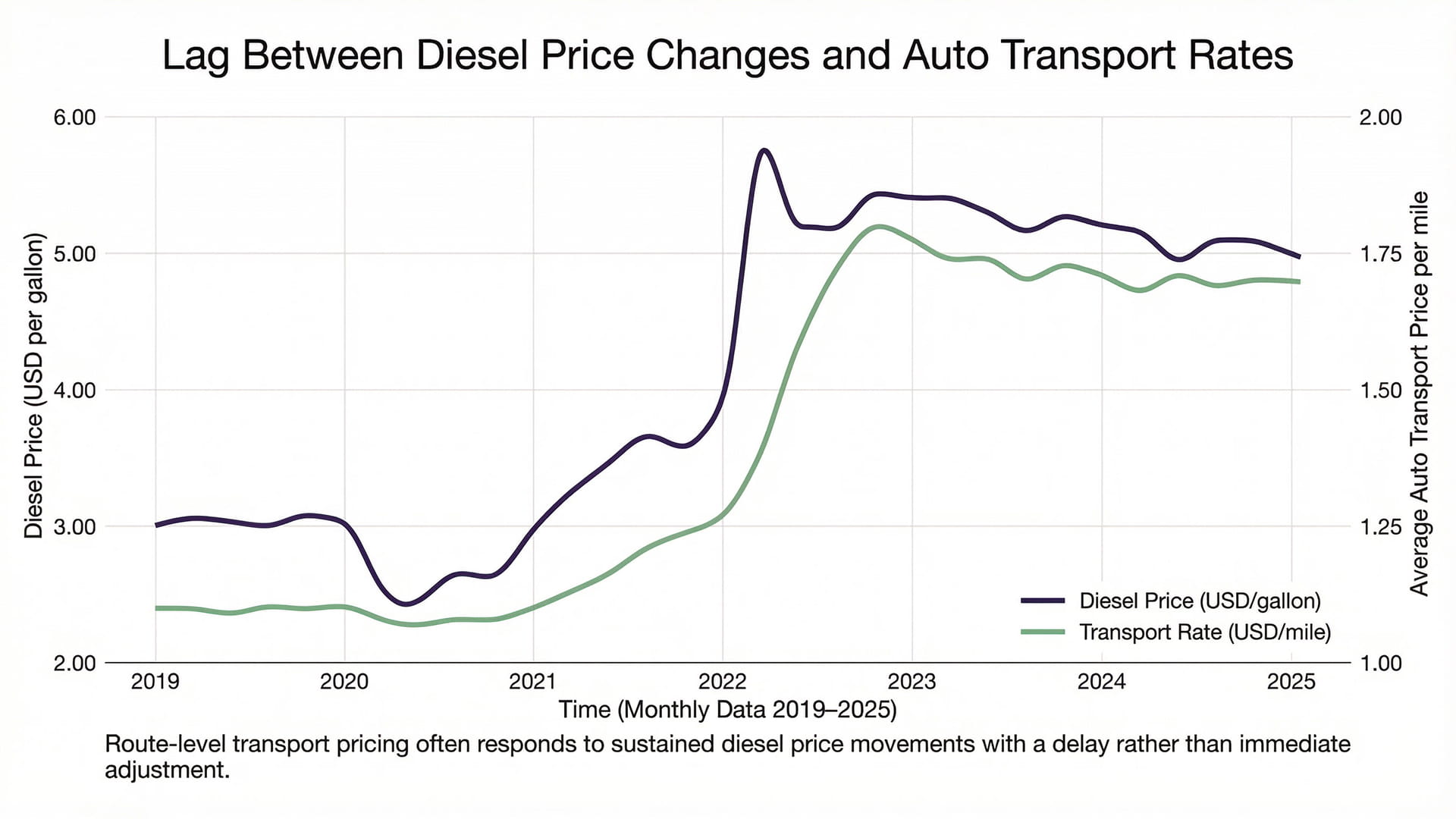

Lag Between Diesel Prices and Auto Transport Rates

A common assumption in vehicle shipping is that transport rates rise immediately when diesel prices increase. However, our analysis shows the relationship is usually slower.

Using monthly averages from EIA diesel price data, we compared fuel movements with route-level pricing across the Texas–Florida, New York–Florida, and Texas–California corridors. In doing so, we looked for timing patterns between fuel changes and rate adjustments.

The results show a consistent lag.

When diesel surged in early 2022, national prices climbed from roughly $3.60 per gallon in January to over $5.70 by June, according to the U.S. Energy Information Administration. Transport pricing did rise during that period, but not immediately. In several cases, rate adjustments appeared weeks or even one to two months after sustained fuel increases.

Part of the explanation lies in how the industry operates. Vehicle carriers rarely reprice shipments based on weekly fuel volatility. Dispatch schedules, booked loads, and existing lane agreements mean that price adjustments usually follow operational cycles rather than headline fuel spikes.

At the same time, freight conditions influence the timing. When trucking capacity tightens, carriers can pass higher fuel costs through more quickly. Conversely, when capacity expands, competition slows the adjustment process.

Our route analysis reinforces this pattern. For example, long-haul lanes such as Texas–California reflected diesel increases more directly, while seasonal corridors like New York–Florida showed stronger influence from demand cycles than from fuel changes alone.

Taken together, the data indicates that diesel clearly matters. But timing and market conditions ultimately determine how quickly fuel costs translate into vehicle shipping rates.

Key Findings & Industry Implications

Our analysis of diesel prices, freight indicators, and route-level transport pricing between 2019 and 2025 shows that fuel is an important cost component in vehicle shipping, but it rarely operates in isolation. Instead, diesel interacts with freight demand, carrier availability, and route distance to shape how transport rates evolve across different corridors.

Several patterns emerged consistently across the datasets:

- Diesel price spikes increase operating costs most noticeably on long-haul routes, where fuel consumption compounds over distance. Corridors such as Texas–California showed stronger fuel sensitivity than shorter lanes.

- Transport pricing typically adjusts with a delay rather than immediately following diesel movements. During the 2022 fuel surge, route-level pricing increases often appeared weeks after sustained diesel increases.

- Freight capacity conditions influence how quickly fuel costs pass through into transport rates. When trucking capacity tightens, carriers adjust pricing faster; when capacity expands, competition slows that process.

- Seasonal demand cycles can outweigh fuel effects on certain routes. For example, New York–Florida pricing during snowbird migration periods increased even when diesel prices remained relatively stable.

Taken together, these findings suggest that diesel remains a major cost factor in vehicle shipping, but the diesel price impact on auto transport costs ultimately depends on distance, timing, and broader freight market conditions.

Limitations of the Analysis

This analysis focuses on diesel price movements, freight indicators, and pricing trends across three major transport corridors. While these datasets capture many of the forces shaping vehicle shipping costs, they do not represent every factor that can influence pricing in real-world shipments.

Conditions such as severe weather, regulatory changes, temporary driver shortages or unexpected supply chain disruptions can affect carrier availability and create short-term price fluctuations that fall outside broader market trends.

At the same time, the route-level pricing used in this analysis reflects averages across multiple shipments rather than individual carrier quotes. Actual pricing may vary depending on vehicle type, pickup timing, service level, and route accessibility.

For that reason, the findings presented here should be viewed as market patterns and structural trends, not exact predictions for individual shipments.

References

[1] EIA Weekly Gasoline & Diesel Update

https://www.eia.gov/petroleum/gasdiesel/

[2] EIA Historical Retail Diesel Prices

https://www.eia.gov/dnav/pet/pet_pri_gnd_dcus_nus_w.htm

[3] EIA Monthly Diesel Price History

https://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=pet&s=emd_epd2d_pte_nus_dpg&f=m

[4] FRED Diesel Price Series (GASDESW)

https://fred.stlouisfed.org/series/GASDESW

[5] FRED Freight-Related Series

https://fred.stlouisfed.org/tags/series?t=freight

[6] BTS Record-Breaking Motor Fuel Prices (2022)

https://www.bts.gov/data-spotlight/record-breaking-increases-motor-fuel-prices-2022

[7] BLS Transportation Service Price Indices

https://www.bls.gov/web/ximpim/srv1.htm

[8] BLS Unit Labor Cost Indexes

https://www.bls.gov/charts/productivity-service-providing-industries/unit-labor-cost-indexes-by-industry.htm

[9] Cass Freight Index

https://www.cassinfo.com/freight-audit-payment/cass-freight-index

[10] ATA Truck Tonnage Index

https://www.trucking.org/economics-and-industry-data/truck-tonnage-index